As the current 2023 year comes to an end, Indigo has rounded up the changes made to tax legislation over the last year that may affect your business. This will help you to get prepared and organised ahead of the next financial year.

April 2023 - Changes to Corporation Tax

Changes on 1 April 2023 meant there was no longer a single Corporation Tax for non-ring fence* companies. Corporation Tax now depends on how much taxable profit a company makes.

For companies with profits above £250,000, Corporation Tax has risen to 25%. Companies with profits of £50,000 or less face a small profits rate of 19%. Profits between £50,000 and £250,000 pay tax at the main rate, reduced by marginal relief.

Marginal relief provides a gradual increase in Corporation Tax rate between the small profits rate and the main rate.

*A ‘ring fence’ company makes profit from oil extraction or oil rights in the UK or UK continental shelf – there are different Corporation Tax rates for these companies.

May 2023 - HMRC VAT online account changes

From 15 May 2023, HMRC changed the way VAT register businesses keep VAT records. This must now be done digitally and VAT returns submitted to HMRC using Making Tax Digital (MTD) compatible software.

Businesses can no longer file VAT returns using any other system. There may be a penalty if VAT returns aren’t filed on time via Making Tax Digital compatible software.

August 2023 - HMRC interest rate changes for late or early payments

From 22 August 2023, the HMRC current late payment and repayment interest rates are:

- Late payment interest rate: 7.75%

- Repayment interest rate: 4.25%

November 2023 - Autumn Statement Tax Announcements

On 22 November 2023, the Chancellor announced a number of tax changes in the Autumn Statement.

- Construction Industry Scheme (CIS) Reform

VAT will be added as part of the Gross Payment Status (GPS) compliance test, which gives HMRC more power to remove GPS immediately in cases of fraud. Contractors and subcontractors will have to undergo VAT record scrutiny as a statutory component of the CIS compliance evaluation.

- Full Capital Expensing Regime

The temporary full expensing regime will be made permanent. This will allow businesses to deduct the full cost of qualifying capital assets from their taxable profits in the year of purchase.

- Tax Deductions on Training Costs

HMRC will rewrite guidance around the tax deductibility of training costs for sole traders and the self-employed, to provide more clarity to businesses on what costs are deductible.

- IR35 Legislation

HMRC plans to reduce the PAYE liability of a deemed employer to account for taxes paid by a worker and their intermediary on payments received where and an error has been made in applying the off-payroll working rules.

- Tax Avoidance Measures

Plans were confirmed to introduce a criminal offence for promoters of tax avoidance who continue to promote avoidance schemes after receiving a Stop Notice. A new power will also be introduced for HMRC to bring disqualification action against directors of companies promoting tax avoidance. Those committing the most serious forms of tax fraud will now be faced with a doubling prison sentence of up to 14 years.

You can read a full summary of the highlights and challenges on Indigo’s Autumn Statement blog here.

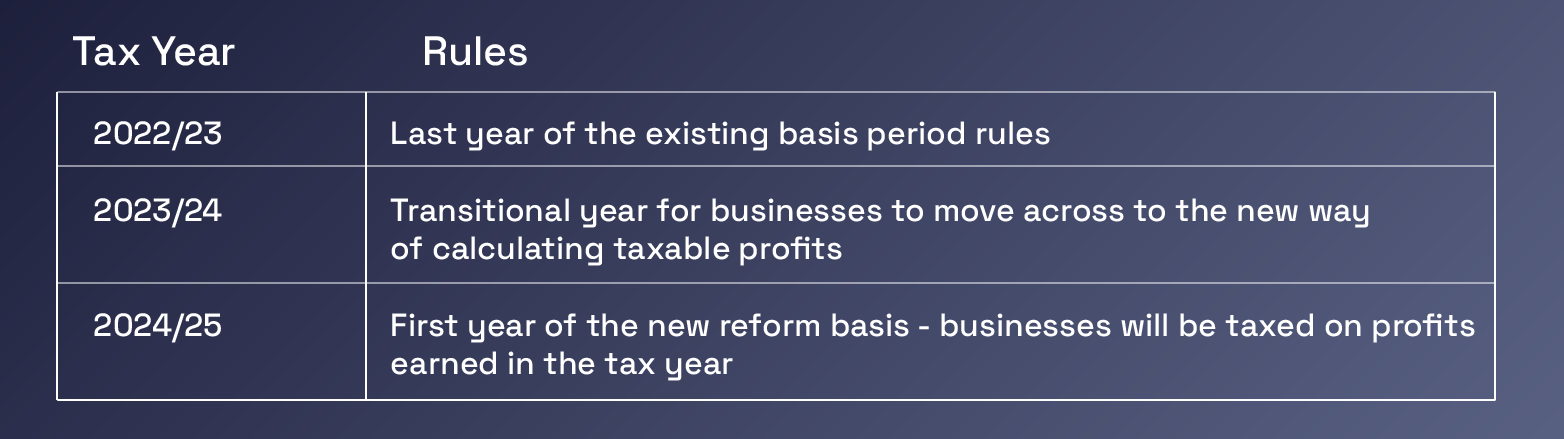

April 2024 - Basis Period Reform: preparing for the new tax year

The way taxable profits are reported and how tax returns are prepared is changing from 6 April 2024. This change will affect self employed sole traders and partnerships with an accounting period between 6 April and 30 March. This change is called basis period reform.

Accounting periods between 31 March and 5 April will not be affected by the change.

Basis period reform means all self employed sole traders and partnerships will report tax to HMRC on a tax year basis, from 6 April to 5 April, regardless of their accounting period.

This change comes into place from the next tax year on 6 April 2024.

HMRC is allowing businesses that use any accounting period and with unused overlap relief to use it during the transitional year. The overlap relief will be ‘lost’ if it is not used before 5 April 2024.

If the basis period reform affects you, there is still time to consider changing your accounting date to 31 March or 5 April, to align your accounting period with the end of the tax year. HMRC has lifted the restrictions on changing your accounting date, starting from the tax return for 2023 to 2024.

Next Steps…

We know that understanding tax can be complicated, but it’s important to get prepared for the new financial year.

If you have any further questions, or would like to speak to someone in more detail, Indigo has a team of in-house experts that will be happy to help! Get in touch.