A Guide to the VAT domestic reverse charge in the construction industry

25/04/2023The Indigo Group

It is now two years since the VAT Domestic Reverse Charge (DRC in short) was introduced into the construction industry in March 2021.

It is a complex area, so we have put together this handy guide to help you understand exactly what DRC is and what it means for you.

Its purpose is to prevent fraud and increase tax compliance in the construction industry.

Under the domestic reverse charge, the responsibility for paying VAT on certain construction services is shifted from the supplier to the customer. This means that the customer must account for the VAT on their own VAT return, rather than paying the supplier.

The reverse charge applies to supplies of construction services made between VAT-registered businesses where the recipient intends to make an onward supply of the construction services. The reverse charge applies to a wide range of construction services, including building, alteration, repair, demolition, installation, and decoration.

There are some exceptions to the reverse charge, including supplies to end-users and supplies of certain professional services, such as architects’ services.

The introduction of the domestic reverse charge has been controversial in the construction industry, with some businesses expressing concern about the administrative burden and potential cash flow issues. However, HMRC insists that the measure will help to reduce the level of VAT fraud in the industry and increase tax compliance. Only time will tell on that one.

This handy flowchart will help you decide where and when the VAT domestic reverse charge applies.

The list of building and construction services affected by the reverse charge is the same as the list of ‘construction operations’ covered by the Construction Industry Scheme (except for supplies of workers provided by employment businesses).

The reverse charge must be used for the following services:

The reverse charge is only applicable to construction companies that are VAT-registered, within the Construction Industry Scheme (CIS) and supplying construction services to another VAT-registered business.

If the customer is a member of the public, the reverse charge does not apply and VAT should be charged to the individual as normal.

The reverse charge is also not applicable to supplies made to an end user. An end user is someone who receives a construction service but does not supply it on, for example, a person owning a property having construction work done to the property.

Further exceptions to the reverse charge also include supplies between connected parties and supplies between landlords and tenants (if the customer notifies the supplier that the exemption applies).

Lastly, supplies by employment businesses or umbrella companies are not subject to the reverse charge, even if those supplies fall within the Construction Industry Scheme. For VAT purposes, employment businesses supplying construction workers are treated as supplying staff rather than building and construction services.

If the reverse charge does not apply, then normal VAT rules should be followed.

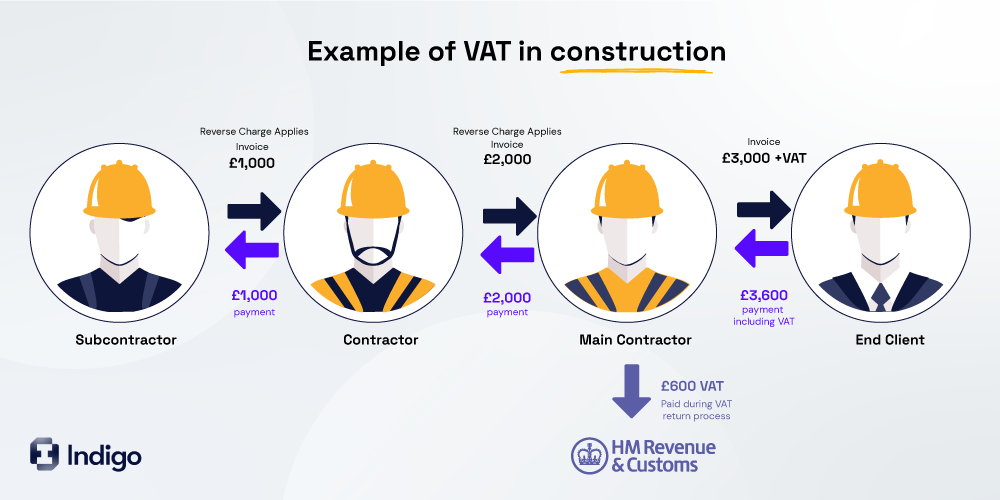

And here is an illustration to help you understand the flows in practice.

When supplied on their own, the following building and construction services are not affected by the reverse charge:

The introduction of the reverse charge has had a huge impact on how businesses in the construction sector manage their VAT and cash flow.

Businesses need to ensure accounting systems and software can deal with the reverse charge and invoices comply with the rules. All staff responsible for VAT accounting should be familiar with the reverse charge and how it works.

The reverse charge may also mean your business could make net repayment claims to HMRC, as you will not receive VAT on payments from customers. You can apply to move to monthly returns using your HMRC online VAT account.

If you are a subcontractor, and the reverse charge applies, then this means customers will not be paying your VAT. This will reduce the gross value of payments coming into your business, so it’s important to plan this into your day to day cash flow.

If you are a supplier, the HMRC recommends checking the CIS and VAT status of your customers to understand whether the reverse charge will apply.

If you are an end user, you may need to provide evidence to the construction business supplying you with services that you are an end user. It is good practice to have this in writing between both parties.

Indigo has a team of in-house experts who will ensure you are complying with the correct VAT rules, including whether the reverse charge applies to you or not.

We will do the hard work, which means you can relax in the knowledge you are compliant and protecting yourself.

Related posts