For self-employed workers and limited companies

Introduction

There are various penalties HMRC issues when tax rules are not followed. Understanding what the penalties are and how they work can help to avoid them.

This guide focuses in more detail on HMRC’s late filing penalties for self-employed workers and limited companies.

What exactly are HMRC penalties?

Penalties are issued by HMRC when tax rules are not adhered to, for example;

- Paying tax late

- Submitting a tax return or other paperwork late

- Failing to tell HMRC about changes that may affect tax liability

- Making an error on a tax return, payment or other paperwork that understates or misrepresents tax liability (unless reasonable care was taken)

HMRC issues a Penalty Explanation Letter which details what penalty is being charged and for what period of time.

How do HMRC late filing penalties affect the self-employed and limited companies?

Self-employed workers have an obligation to submit a Self Assessment tax return, along with any payments for Income Tax and National Insurance Contributions that are reported on that tax return. These submissions are required by the deadline date of 31 January (paper tax returns are due earlier by 31 October).

If the deadline is missed by one day for Self Assessment tax returns, a fixed £100 late filing penalty will be issued by HMRC. This penalty will still be applied even if there is no tax owed.

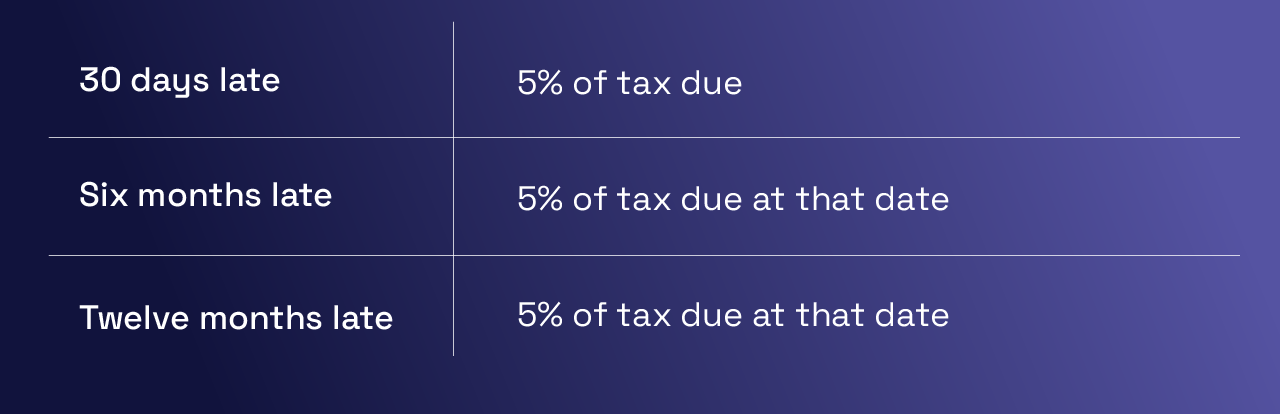

After three months, the penalties increase and are as follows:

Late payments for Income Tax and National Insurance Contributions incur separate penalties in addition to the above penalties for late tax returns.

There is an additional 3% interest on the above penalties for overdue taxes until the bill is paid in full.

What about contractors under the Construction Industry Scheme (CIS)?

Contractors under the Construction Industry Scheme (CIS) face additional late filing penalties if the deadline for submitting CIS returns is missed.

An automatic fixed penalty of £100 will be issued if the return is missed by one day. Following this if the return is still not received, penalties listed below will be issued:

After twelve months, the penalty is either £300 or 5% of CIS deductions (whichever is higher) or if HMRC discovers information was deliberately withheld, a ‘higher’ penalty will be issued.

The higher penalty can be up to 100% of any liability to make payments, or a minimum penalty of £1,500 or £3,000.

Penalties can be cancelled by HMRC if a contractor did not pay subcontractors during that month. However, the contractor is responsible for letting HMRC know.

Appealing against late filing penalties

All taxpayers have the right to appeal against any late filing penalties they disagree with. HMRC will only accept an appeal after they have received a late tax return. Appeals must be sent before 30 days of the date of the penalty notice (unless the notice gives a new date).

HMRC has a list of ‘reasonable excuses’ they may consider when reviewing an appeal. According to HMRC, a reasonable excuse is ‘something that stopped you meeting a tax obligation that you took reasonable care to meet’. As soon as a reasonable excuse is resolved, HMRC expects the outstanding late filing to be met.

The list from HMRC includes:

- a partner or another close relative died shortly before the tax return or payment deadline

- an unexpected stay in the hospital that prevented you from dealing with your tax affairs

- a serious or life-threatening illness

- computer or software failed just before, or while you were preparing your online return

- HMRC online service issues

- a fire, flood or theft prevented you from completing your tax return

- postal delays that you could not have predicted

- delays related to a disability you have

HMRC will not accept the following as a reasonable excuse:

- relying on someone else to send your return and they did not

- cheque bounced or payment failed because you did not have enough money

- the HMRC online service is too difficult to use

- did not get a reminder from HMRC

- made a mistake on your tax return

How can Indigo help?

Don’t get caught out by late filing penalties and plan ahead of tax deadlines.

Indigo makes sure that your financial paperwork is meticulously maintained and securely stored on our platform, minimising administrative tasks when collaborating with subcontractors to avoid delays in tax returns.

To find out more about our ‘Contract’ solution here