IR35 or the “off-payroll working rules” were extended into the private sector in April 2021. From this date, the IR35 rules became relevant for contractors working through personal service companies (PSCs) in the private sector.

IR35 can be a complicated topic, so we’ve put together this guide to answer some of the most frequently asked questions and to help contractors in the private sector understand the changes to the IR35 rules that came into place in April 2021.

What exactly is IR35?

IR35 is a UK tax legislation that ensures contractors cannot avoid paying the correct tax by working as “disguised” employees.

Under the IR35 rules that came into place in April 2021, clients and end users of contractors working through personal service companies (PSCs) are now required to assess whether the contractors work like employees. This ensures contractors pay broadly the same National Insurance (NI) and income tax contributions as a company employee would.

Each contract needs to be considered individually for IR35 status, as some may fall within the IR35 rules and some outside. A contract for the purpose of IR35 is a written, verbal or implied agreement between parties.

How is IR35 status determined?

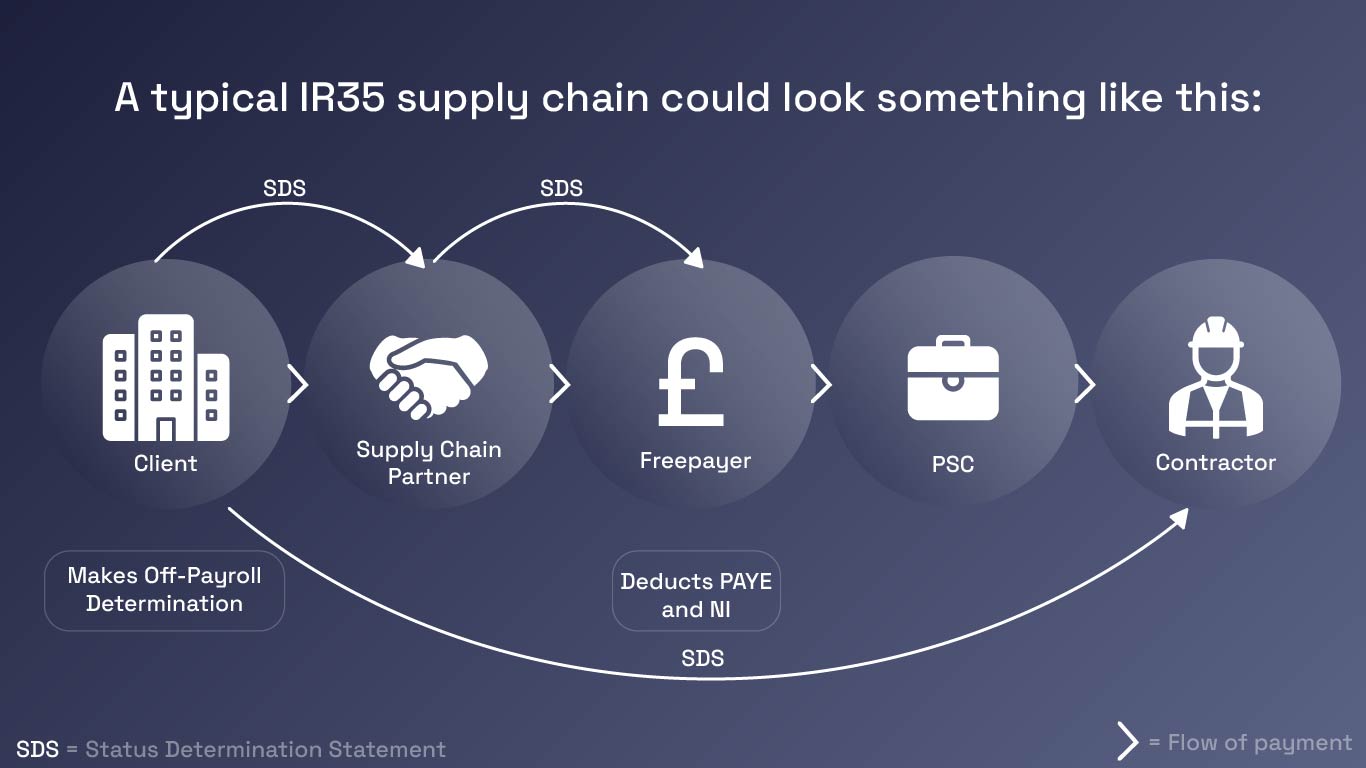

Contractors will receive a “Status Determination Statement” (SDS) from the client or end user. Depending on the contract and working arrangements, the SDS will deem a contractor either “inside” or “outside” IR35 rules. Contractors can dispute the IR35 decision with clients or end users if they do not agree.

HMRC regards contractors that are “inside IR35” as employees for tax purposes. Contractors “outside IR35” are seen as “genuinely” self-employed by HMRC which means they are able to operate tax efficiently.

What does inside IR35 mean?

If a contractor is deemed to be inside IR35, they are employed and must pay income tax and National Insurance (NI) the same as employees.

The client or end user of a contractor’s PSC (usually the fee-payer) will deduct tax and NI before paying the contractor for services provided.

What does outside IR35 mean?

If a contractor is deemed to be outside IR35, HMRC considers them to be operating as a genuine business and therefore operating outside of the IR35 rules. The responsibility for paying the correct NI and tax contributions falls directly to the contractor when outside IR35.

The client or end user of a contractor’s PSC (usually the fee-payer) will not deduct tax and NI before paying the contractor for services provided.

Inside or Outside IR35?

There are some factors that can indicate whether a contractor is inside or outside IR35. Below is a non-exhaustive compliance checklist for contractors:

New rules explained

IR35 Timeline

2000: IR35 rules are first introduced. Contractors are responsible for assessing their own IR35 status.

2017: Changes to the IR35 rules for the public sector. The public sector body engaging contractors is now responsible for assessing contractor’s IR35 status.

2021: Changes to the IR35 rules for the private sector. To align with the public sector rules, private sector businesses engaging contractors are now responsible for assessing IR35 status of contractors.

As of April 2021, contractors in the private sector are no longer responsible for assessing their own IR35 status. This change aligns the IR35 rules across the public and private sector.

Clients or end users of PSC are responsible for assessing the IR35 status of contractors and will provide a “Status Determination Statement” (SDS) with their decision of whether a contractor is inside or outside IR35.

IR35 checklist: everything you need to know

- The PSC will no longer be responsible for determining if IR35 applies

- End users and clients must assess IR35 status for each engagement, ensuring they take reasonable care in doing so

- End users and clients must put in place a status determination disagreement process

- If ‘inside IR35’ the fee payer must deduct tax and NI before paying the PSC

- If ‘outside IR35’ the fee payer will not deduct tax or NI before paying the PSC and this responsibility falls to the PSC to deduct the correct amounts

- HMRC can pass tax liability up the supply chain if the rules are not followed with reasonable care

How can Indigo help?

Indigo can run an IR35 check to any company that may be at risk from being misclassified.

For more information about working with Indigo, get in touch below.